High debt balances, multiple cards, different due dates, high stress levels, ugh! Having multiple sources of debt can feel really overwhelming.

You may have been making debt payments for a long time, but your balances are still going up. You might even be considering… *whispers* bankruptcy. Before we go there, many people consider debt consolidation first.

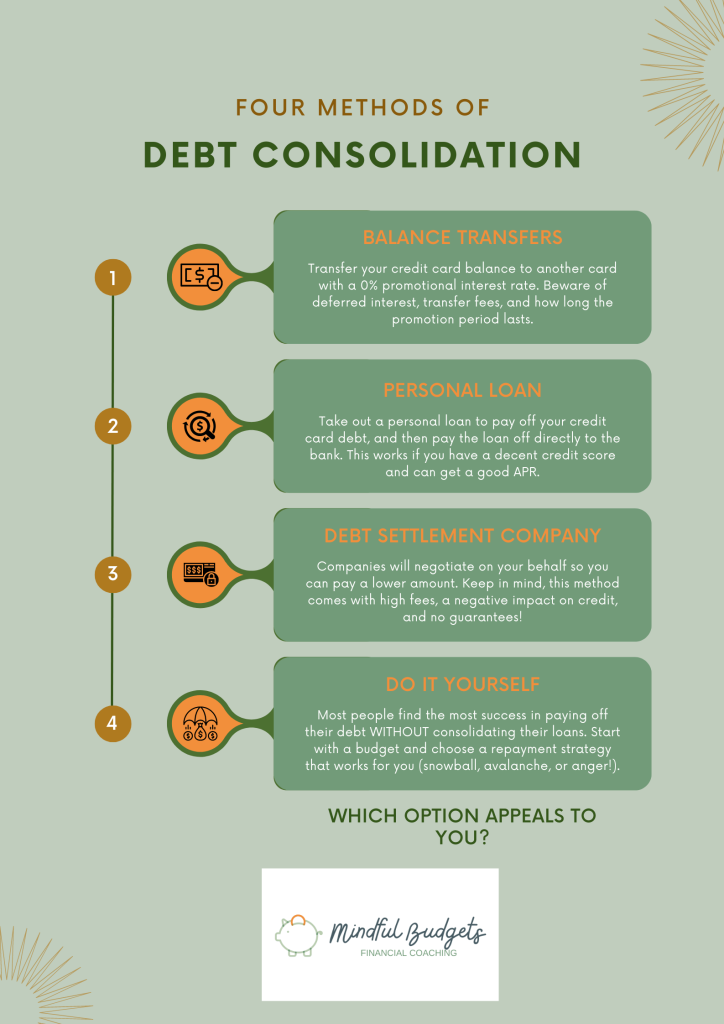

What is debt consolidation?

Debt consolidation is the process of combining two or more debt accounts into one. If you have multiple credit cards, it might mean you take out a single loan to pay off all your cards, then you just have to worry about one personal loan payment instead.

Simplifying your payments can’t be bad, right? But debt consolidation doesn’t always make things easier. Though making one payment instead of five seems like less paperwork, but that alone doesn’t mean it’s the best option for everyone.

There are a few ways to approach debt consolidation, and each method has it’s own pros and cons. Let’s review them to see what might work best for you.

Method 1: Balance Transfers

Have you seen those 0% balance transfer offers that credit cards offer? This will allow you to transfer the balance you have on one card to another, and a lot of times, banks will offer you a limited promotional interest rate (as low as 0%) in order to entice you to switch.

Credit card companies LOVE to do this, because it gets you in deeper with them. And it doesn’t seem like a bad deal, because you get to lock in a lower interest rate as you pay down your debt. Just keep in mind a few caveats:

- Limited time-frame: promotional interest like 0% will usually last between 12 or 18 months, which means you need to pay off the entire balance on the card before that time period ends, otherwise your balance gets charged with a very high interest rate (usually 24% or higher).

- Transfer fees: most banks will immediately charge you a percentage of the balance you’re transferring (usually between 2-4%) so be sure to factor that extra cost in, to decide whether it’s worth switching over. This can be hundreds of dollars of extra fees.

- Deferred interest: most balance transfer deals include a “deferred interest” clause. This means that you are still accruing interest on your balance during the whole promotional period. When the promotional period ends, you will be charged all the interest that has snowballed for the past 12-18 months. You won’t be charged if you fully pay off your balance before the promotional period ends, but many people falsely believe that the promotional period is interest-free when in reality, it’s only deferred to later.

If you feel highly confident in your ability to pay off the entire balance on a card before the promotional period ends, a balance transfer can be an effective tool. I recommend that you only transfer the amount you can confidently pay off, and ensure that the interest rate + balance transfer fee are less than the interest you would pay if you just left the balance where it already is.

Method 2: Personal Loan

Getting a personal loan is another valid way to consolidate your debt. You get a loan from a bank, use it to pay off all your credit cards, then make payments to your bank to pay back the loan. It’s simple, but again, there are factors to consider here.

- Credit score: You need a fairly decent credit score to get approved for a personal loan, and most people considering debt consolidation often don’t have the best credit score, especially if you’ve been struggling with making payments on your debt. In those cases, it may be pretty hard to be approved for a loan.

- Interest rate/APR: Using a personal loan to consolidate your debt only makes sense if you can get a lower APR on the loan than you have on your credit cards, which depends again on your credit score and payment history. It’s important to do the math here to decide if the loan terms are actually better than the credit card terms.

- Spending urges: This method may not be the best for people who are having trouble restraining their urge to spend. Using a personal loans means all of your credit limits are cleared up for more spending, and that might be too tempting for you to resist. There are many, many cases of people who take out a loan to pay off their cards only to rack up more credit card debt because they haven’t been able to address the root issue of their spending.

If you have a good credit score and don’t struggle with impulsive spending, a personal loan can fast-track your road to being debt-free with lower interest rates and a simplified payment.

Method 3: Debt Consolidation Companies

Finally, there is an option to work with a debt consolidation company who specialize in debt settlement. It probably sounds amazing to let someone else manage all the messy details, but let’s be clear on how it works.

The company will ask you to stop paying all your debts and instead, pay into a special savings account. Once there’s enough money saved, the company takes that money and negotiates with your creditors to pay a lower balance than what you owe (normally, much lower). Sounds good, so what are the downsides?

- Fees. The company will charge you a fee for this service, which can be as high as 25% of your total debt.

- Credit score impact: By following their methods and not paying your debt temporarily, you’re effectively defaulting on your loans, so your credit score will plummet further (hopefully temporarily).

- No guarantees: This process does not always work! There are no guarantees. If the company can’t reach an agreement with one or more of your creditors, you’ll still be responsible for paying the full amount of your debt PLUS any accrued interest or fees from not paying your debt this whole time. You’re out the fee you paid the consolidation company, and you retain all the damage done to your credit. So it’s possible that you may be left worse off than you started.

If you’re okay with an impact on your credit score, risk, and you just want to hand off the reins to someone else, a debt consolidation company might be able to ease your burden.

Method 4: Don’t Consolidate

If none of these options sound good to you, here’s the good news.

Many people actually have greater success by not consolidating their debt.

It sounds nice to simplify your payments and gain a better interest rate, but the psychological effect of having a huge looming balance can be really intimidating, discouraging, and hopeless.

By keeping balances separate, you can gamify your debt payments and get a feeling of accomplishment and pride by making more significant progress towards smaller balances. Every closed account will go a long way to keeping you motivated.

Here are a few other considerations if you decide to go this route:

- Hardship programs: If you’ve experienced a hardship (job loss, illness, pay cuts, family emergencies), you may qualify for your creditor’s hardship program. If you can provide documentation, many creditors will lower your monthly payment and interest rates. This way you don’t have to worry about defaulted accounts or pay a company to negotiate for you — you can do it yourself, directly with the creditor. Just keep in mind that sometimes creditors will lower your credit limit or close/freeze your accounts, and if that results in a higher credit utilization ratio, your credit score may be impacted.

- Debt repayment strategies: There are a few different strategies to pay off your debt: snowball, avalanche, or anger are just a few. Going your own route allows you the flexibility to do what works for you.

- Start with a budget: It can be tough to pay off your debt (and stay out) if you’re not clear on what habits caused the debt in the first place. Get a clear picture of the amount of money coming in and going out, and start your debt repayment journey with getting a clear budget in place. This will future-proof your debt strategy so you can stay out now and forever.

Which method appeals to you? Do you have experience with using any of these methods to consolidate your debt? Let us know in the comments.